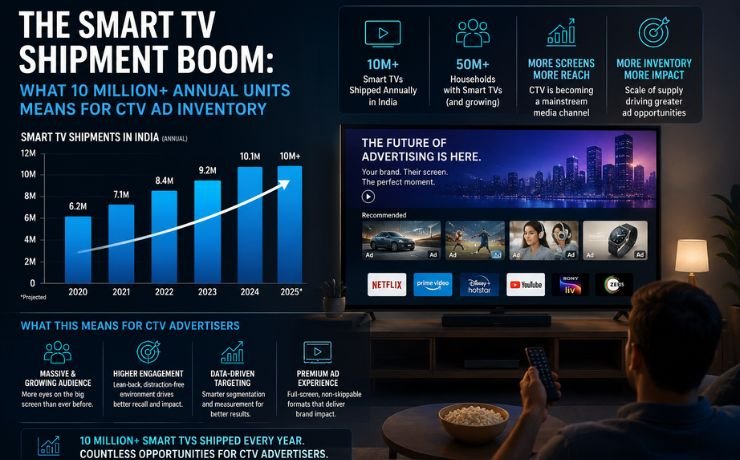

The Smart TV Shipment Boom: What 10 Million+ Annual Units Means for CTV Ad Inventory

Somewhere in a warehouse outside Chennai, a container of smart TVs is being unloaded right now. It will not be the last one this quarter, and it will not be the biggest. India’s smart television market has quietly crossed a threshold that advertisers spent the better part of a decade waiting for — annual shipments north of 10 million units, sustained not as a festive-season spike but as a structural baseline. For an industry that has long treated connected TV as the promising younger sibling of digital advertising, this is the moment the sibling gets its own seat at the table.

The number itself deserves a pause. Ten million smart TVs is not simply a retail statistic. It is ten million new potential nodes in a household’s media diet, each one arriving pre-loaded with an operating system, an app store, and — crucially for anyone in the business of reaching audiences — a data pipe back to an ad server. Every unit sold is a small, silent expansion of programmatic inventory that did not exist in that form a year ago. And unlike a smartphone upgrade cycle, a television purchase tends to anchor a household’s primary screen for the next five to seven years, which means the industry is not looking at a temporary bump but at the slow, compounding replacement of India’s living room glass.

From Appliance to Ad Platform

It is worth remembering how recently this shift happened. For most of the last decade, the television in an Indian home was exactly what it sounds like — a dumb panel connected to a cable box or a satellite dish, entirely deaf to programmatic bidding, entirely blind to a user ID. The smart TV changed that arithmetic by folding the operating system directly into the hardware. Suddenly the television was not a passive display but an addressable endpoint, capable of running its own apps, surfacing its own recommendations, and — this is the part that matters to media planners — carrying its own advertising ID, not unlike the one sitting quietly inside every smartphone.

What has made the last eighteen months different is price. Smart TV panels that once carried a premium have collapsed toward parity with basic television sets, aided by aggressive local manufacturing, a crowded field of homegrown brands competing on margin rather than markup, and a consumer base that increasingly refuses to buy a non-smart set even when it costs less. The result is a market where “smart” has stopped being a feature and become the default. When a category tips like that, the advertising implications stop being theoretical.

Every television that leaves a warehouse with an operating system attached is, whether the household realises it or not, a future line item in a media plan.

The Inventory Math Nobody Has Fully Solved

Here is where the optimism needs a companion dose of realism. More smart TVs in circulation does not automatically translate into more usable CTV inventory — at least not the kind that a performance marketer or a brand safety officer would recognise as clean, addressable, and fraud-resistant. A television is only as valuable to an advertiser as the content running on it, and a meaningful share of newly shipped smart TVs spend their working hours mirroring a smartphone screen, casting a cricket match from a subscription app, or sitting on a home screen full of pre-installed content nobody watches. Shipment volume measures boxes leaving a factory. It does not measure attention.

This is the gap that ad tech vendors, measurement partners, and the smart TV manufacturers themselves are now racing to close. Automatic content recognition, the technology that allows a television to identify what is playing on screen regardless of the source, has become the quiet battleground of this expansion. Without it, a broadcaster or a platform has shipment numbers but no proof of eyeballs. With it, that same inventory becomes something a media buyer can actually plan against — a screen with a verified, timestamped record of what content ran, when, and for how long. The manufacturers who get ACR right, and who strike the right data-sharing terms with demand-side platforms, stand to capture a disproportionate share of the ad dollars this shipment boom is meant to unlock. The ones who treat it as an afterthought will simply have sold hardware.

What This Means for the Media Plan

For agencies and brand marketers, the practical question is less “should we buy CTV” and more “how much of the plan should now assume CTV as a baseline, not a bolt-on.” A few implications are already visible in how forward-leaning buyers are behaving.

First, reach calculations are being rewritten. A media plan built eighteen months ago that treated linear television as the reach vehicle and CTV as a supplementary layer for younger, urban audiences is already out of date in tier-two and tier-three markets, where much of this new shipment volume is landing. The smart TV is no longer a metro phenomenon riding on premium broadband; it is arriving in homes on modest data plans, often as the household’s first proper streaming device. That changes the audience composition CTV can credibly claim to represent, and it changes the case for shifting budget away from pure linear toward a blended buy.

Second, frequency capping — long a theoretical nicety in Indian CTV buying because inventory was too fragmented to manage — is becoming operationally realistic. With more households owning a smart TV as their sole or primary screen, and with identity resolution improving across ecosystems, buyers can begin to build genuine household-level frequency logic rather than treating every impression as a fresh, unconnected event. This alone changes the efficiency math on campaigns that previously over-delivered to the same narrow slice of connected households while starving everyone else.

Third, and perhaps most consequential for the format itself, the growing base is forcing a maturation of ad formats beyond the interruptive fifteen-second pre-roll lifted wholesale from YouTube playbooks. Shoppable overlays, QR-driven second-screen activation, and interactive ad units designed specifically for a ten-foot viewing experience are moving from pilot to standard offering, because the audience volume finally justifies the production investment required to build them properly.

The Fragmentation Problem Gets Bigger, Not Smaller

It would be tidy to say that shipment growth simply expands a single, unified pool of inventory. It does not. Every new smart TV shipped carries an operating system chosen by its manufacturer, and India’s smart TV market is unusually fragmented across a handful of competing platforms, each with its own app ecosystem, its own data policies, and its own relationship — or lack of one — with the programmatic supply chain. A buyer trying to plan reach across this landscape is not solving one inventory problem; they are solving it separately for each operating system, each with different levels of transparency about who is actually watching.

This fragmentation is, paradoxically, one of the more interesting opportunities buried in the shipment numbers. Operating system providers that can offer the cleanest data, the most transparent supply path, and the fewest intermediaries between advertiser and screen are positioned to command a premium over rivals selling comparable reach but murkier provenance. Expect consolidation pressure here over the next eighteen months, as smaller platforms either strike aggregation deals with larger demand-side players or find themselves relegated to remnant inventory nobody wants to plan against directly.

Measurement Is Still the Unfinished Business

No conversation about CTV inventory growth in India is complete without acknowledging the elephant sitting on the sofa: measurement standards remain inconsistent across the ecosystem, and no single currency has emerged that commands the trust linear television ratings once did. Different platforms report reach and completion rates using different methodologies, making cross-platform comparison an exercise in approximation rather than precision. For an industry moving real budget, that is not a footnote — it is the single biggest brake on how fast this shipment boom converts into ad revenue.

The organisations best positioned to benefit from the next phase of growth will not necessarily be the ones shipping the most units. They will be the ones willing to invest in third-party verification, in transparent viewability standards for the ten-foot screen, and in measurement partnerships that give buyers a reason to trust the numbers enough to move budget at scale rather than testing cautiously at the margins. Trust, in this business, has always been the real currency, and television — even smart television — has not yet fully earned it in its new digital form.

The Longer Arc

Step back far enough and the shipment boom looks less like a single headline and more like the opening chapter of a longer story about how Indian households consume media. A decade ago, the defining shift was the smartphone turning every individual into an addressable audience of one. What is happening now is the household catching up — the living room television, for so long the last analogue holdout in a digitised media diet, finally becoming as legible to advertisers as the phone in every family member’s pocket.

That legibility will not arrive evenly, and it will not arrive without friction. Fragmented operating systems, inconsistent measurement, and inventory that looks impressive on a shipment chart but thinner on an actual audience report will all continue to complicate the picture for the next few buying cycles. But the direction of travel is no longer in question. Ten million units a year is not a ceiling; industry watchers increasingly treat it as a floor, with growth continuing to compound as replacement cycles kick in and price points fall further. For anyone planning a media budget in this country, the smart TV has stopped being an experimental line item and started being infrastructure — the kind you plan around, not the kind you test cautiously at the edges. The inventory is coming, in volumes that make yesterday’s caution look increasingly like a wasted opportunity. What remains to be built is the trust, the standards, and the measurement discipline to make sure that inventory is worth as much as its growing numbers suggest.